|

Fixed Index Annuities

What is an Indexed Annuity?

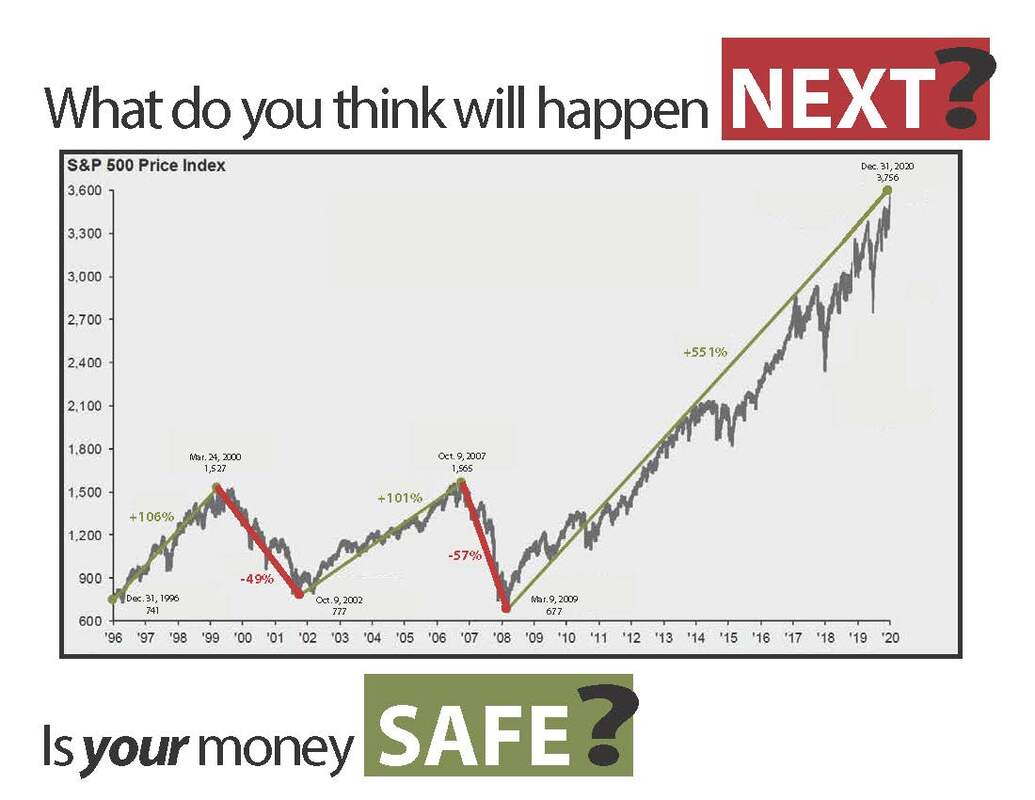

An annuity is a type of life insurance product that's designed to provide you with enough income to stay afloat through your retirement, and the indexed annuity is a more specific kind of annuity for which the returns are based on an equity-linked index. One typically buys an indexed annuity from an insurance company. In the following, you'll find out more about how indexed annuities work and what you might expect in terms of returns. Conservative Investment Plan Compared to other retirement vehicles you might choose, the indexed annuity is a fairly conservative way to save. When one purchases an indexed annuity contract, the contract will be linked to the performance of some stock index, most often the Standard and Poors 500), which acts largely to determine the interest rate. However, the link between the performance of the index and the performance of the indexed annuity can vary greatly depending on the specifics of your contract.

Click to Enlarge

LEARN MORE ABOUT ANNUITIES

|

LEARN ABOUT THE

FOUR TYPES OF ANNUITIES

Index Annuity Links

Here are some of the most popular indexes on the market.

Fixed Index Annuity Potential Benefits

|

What's a state Guaranty Association and how does it work?

Life, health and long-term care insurance, or annuities - the Guaranty Association will pay up to the policy limit, or up to $500,000, whichever is lower.

Life, health and long-term care insurance, or annuities - the Guaranty Association will pay up to the policy limit, or up to $500,000, whichever is lower.

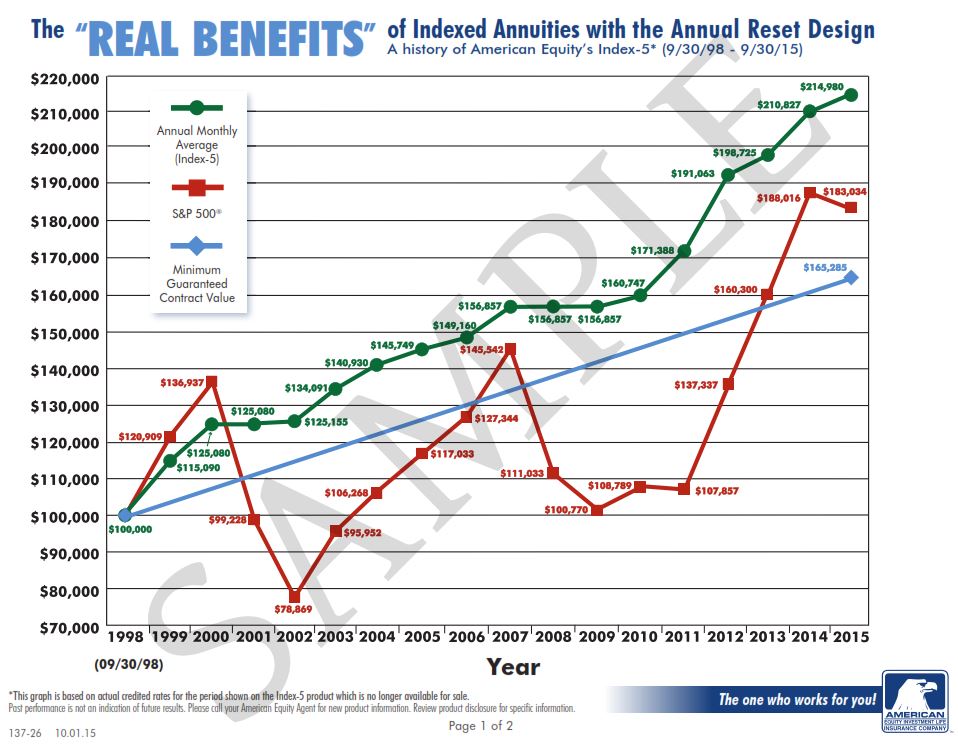

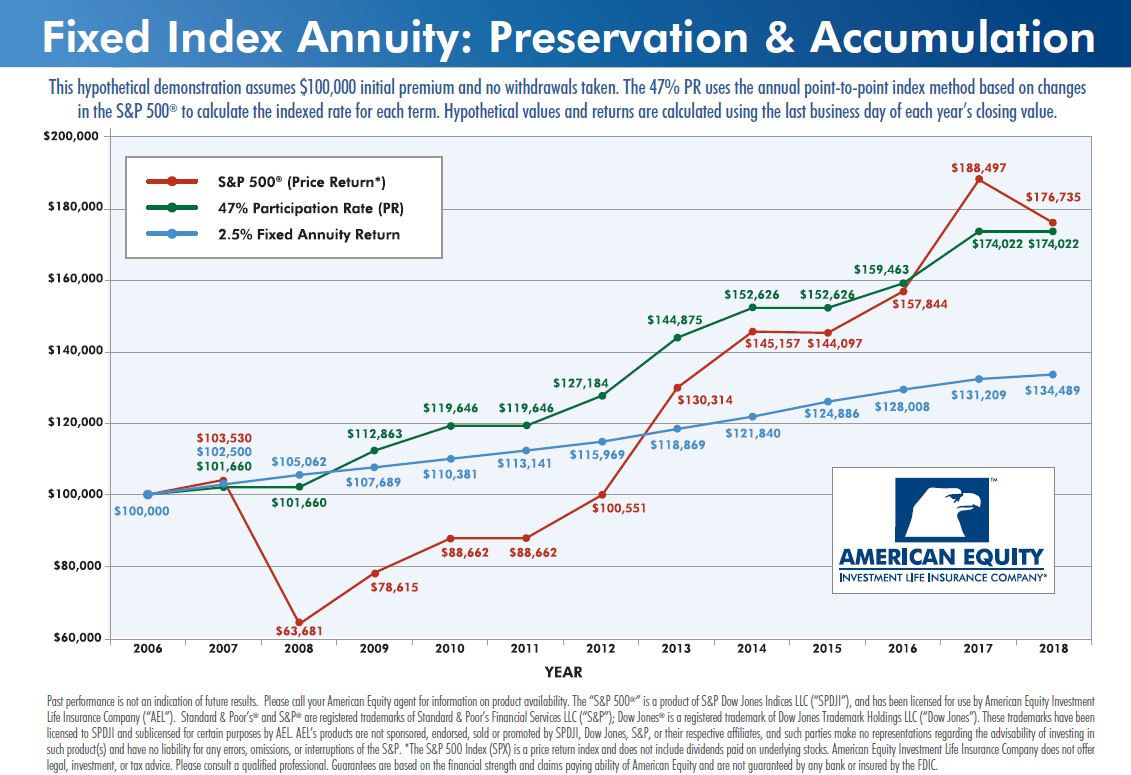

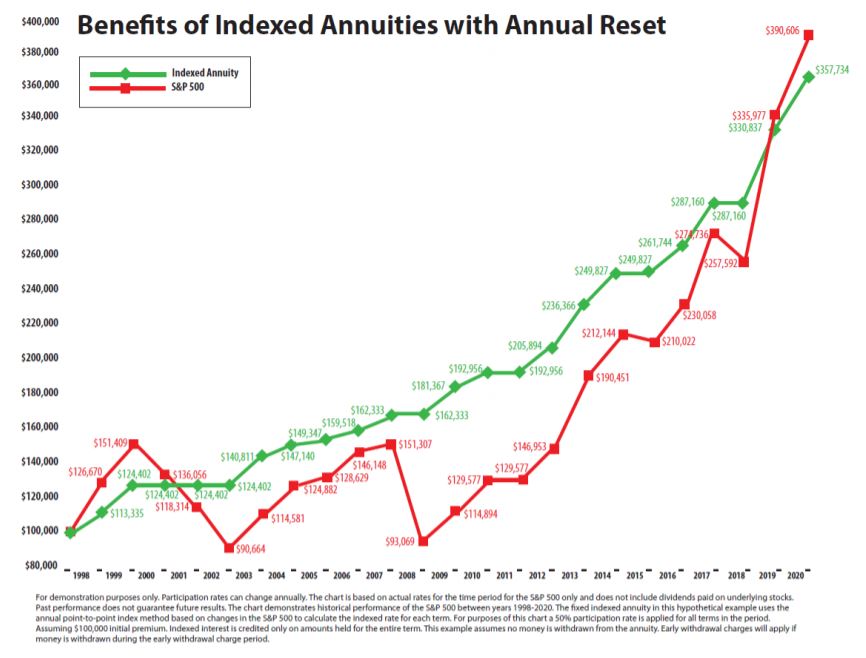

Index annuities are linked to an outside index and help provide the potential for growth when the index rises (without direct exposure to it). When the index rises, your annuity value can increase. When the index goes down, you don’t lose money; it just stays the same. Indexed annuities offer a wide range of guarantees* and growth potential.

|

INDEX ANNUITY PROS

|

INDEX ANNUITY CONS

|

Crediting Methods

How the annuity grows depends upon the annuity you choose. On a growth focused annuity, you will use a participation rate and either a Cap or Spread rate.

HERE ARE EXAMPLES

WANT TO LEARN MORE???

Download these resources

How the annuity grows depends upon the annuity you choose. On a growth focused annuity, you will use a participation rate and either a Cap or Spread rate.

HERE ARE EXAMPLES

- Participation Rate - The Participation Rate is the percentage of any increase in the index value that will be used to calculate the interest credit percentage. For Example: If the Participation rate was 80% and the index made 10%, you would net 8%. This works good in a volatile market and low volatility market depending upon your rate.

- Cap on Growth - Some annuities may put an upper limit, or cap, on the percentage change in the index value. This is the maximum rate of interest the annuity will earn. For Example: If the participation rate was 100% and a had a cap rate of 6% you would receive a maximum of 6%. So if index value was 7.2%, then 6% will be credited not the 7.2%. The higher the cap the better. This works good in a normal market under 10%, but will not capture a great market with high returns due to the cap.

- Spread Cost on Growth - Margin or spread A specified percentage used in certain calculation methods with fixed indexed annuities to determine the amount of index-linked interest that is credited to the annuity. For Example: If the participation rate is 100% and spread cost was 2%, you would get 100% of what the index made less a spread cost of 2%. So if the index made 10% you would subtract 2% and you would receive a net 8%.

WANT TO LEARN MORE???

Download these resources

HOW DO THEY COMPARE???

"ILLUSTRATIONS ARE FOR EDUCATIONAL USE ONLY"

Please ask for your customized Illustration Comparison

"ILLUSTRATIONS ARE FOR EDUCATIONAL USE ONLY"

Please ask for your customized Illustration Comparison

|

GROWTH ANNUITY

This is a sample of a Fixed Index Growth Annuity with no Income rider but strictly used for potential higher returns linked to a market based index offering no risk and in many cases no fees. |

INCOME ANNUITY

(Wait 5 Years for Income) This is a sample comparison between three Fixed Index Annuities with an income rider demonstrating how guaranteed income would pay a lifetime income if a person waits 5 years before taking income. |

INCOME ANNUITY

(Wait 10 Years for Income) This is a sample comparison between three Fixed Index Annuities with an income rider demonstrating how guaranteed income would pay a lifetime income if a person waits 10 years before taking income. |

*** These samples above are examples which may not be current or customized to you. Please ask for your own up to date comparison at no cost. And as always, it’s important to keep in mind that past performance is definitely no guarantee of the future results that you’ll receive in most any financial vehicle.

|

FREE Educational Annuity Books that you can read about different topics, written by Josh Mellberg.

|

|