What is Disability Insurance?

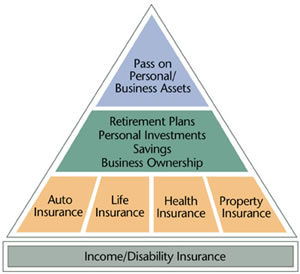

Disability insurance is a form of coverage that will replace a percentage of your income should you be unable to work because of injury or illness. Most policies are written for a specific monthly benefit - the face amount of the coverage. The upper limit is typically between 50% and 70% of your earned income. Disability insurance is also known as paycheck protection or income protection. These products provide replacement income when a breadwinner is unable to work due to illness or injury. Disability insurance is essential coverage for business owners and high-earning professionals.

Are you prepared for a disability?

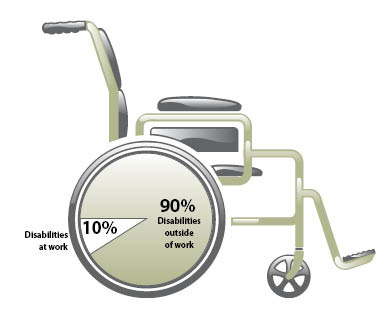

FIVE questions every worker should ask. Illnesses and accidents are on the rise in America, causing more workers to miss work and lose income. At some time during their working careers, three out of every 10 workers will suffer a disability and be unable to work for a significant period of time. Loss of income can be devastating. Today, it’s more important than ever for workers and their families to understand how they would manage their regular expenses during a period of lost income and make sure they’re prepared. To help workers better understand how prepared they are should the unthinkable happen - a loss of income due to an accident or illness - Below are FIVE questions every worker should be asking:

|

|

Types of Disability Insurance

- Individual disability insurance - this type of policy is written specifically for the covered individual, with choices for coverage amounts, periods, exclusions, etc. The more comprehensive the coverage, the higher the cost. Policies are subject to standards of health, age, occupation, etc.

- Group disability insurance through an employer - with employer provided plans, many of the decisions about policy definitions and structure have already been made. Coverage is more readily available to persons with health problems, but coverage stops when employment is terminated.

- Social Security disability benefits - Federal programs that pay benefits to all disabled persons under age 65, and pay supplemental benefits to persons over age 65 who have limited incomes.

- Workers compensation - state mandated coverage that pays benefits for persons disabled because of work related injuries or illnesses

- VA benefits - Federal program that pays veterans who are disabled due to service related health problems

- Federal Employees Retirement System - Program that covers Federal employees and pays up to 60% for the first year and 40%, thereafter.

- State-sponsored coverage - several states (including California, Hawaii, New Jersey, New York and Rhode Island) pay short-term benefits to residents who are disabled due to issues not related to work.

|

Key Definitions

Understanding these terms is critical to purchasing the right coverage

|

|

|

RENEWABILITY POLICY OPTIONS

Residual Rider

Covers you when you are only able to return to work part time. This rider will pay you the difference so you can maintain your lifestyle.

|

Occupation Type

TRUE OWN OCCUPATION

Is best for jobs that require manual dexterity Consider MODIFIED OWN OCCUPATION for jobs not requiring high levels of dexterity |