Choosing Beneficiaries for Your IRA

Like many Americans, you may retire or reach retirement age with an unexpected windfall — a large retirement plan account balance. Whether it’s a 401(k) plan, a defined benefit plan, or some other type of individual retirement plan, your objective in making contributions was to take advantage of the tax-deferral benefits that such plans offer. However, once you reach retirement age, the fruits of your savings are subject to mandatory distribution requirements and possible taxation that many people overlook.

Making sure that you have made plans ahead of time for your retirement assets is crucial to a comprehensive financial and estate plan. Such planning can help ensure that you are able to meet your financial needs after you retire. In addition, should you die before reaching retirement age, you can ensure the financial well-being of your surviving beneficiaries.

The most common vehicle for shifting retirement plan assets at retirement is an individual retirement account (IRA). Upon reaching retirement, you can roll over your retirement plan assets into an IRA. If you die before reaching retirement age or before you establish an IRA account, your designated beneficiary of your retirement plan may be able to roll the assets into an IRA as well. Typically when choosing beneficiaries an IRA owner may name a spouse, child, trust, or charity as a beneficiary of his or her IRA.

Like many Americans, you may retire or reach retirement age with an unexpected windfall — a large retirement plan account balance. Whether it’s a 401(k) plan, a defined benefit plan, or some other type of individual retirement plan, your objective in making contributions was to take advantage of the tax-deferral benefits that such plans offer. However, once you reach retirement age, the fruits of your savings are subject to mandatory distribution requirements and possible taxation that many people overlook.

Making sure that you have made plans ahead of time for your retirement assets is crucial to a comprehensive financial and estate plan. Such planning can help ensure that you are able to meet your financial needs after you retire. In addition, should you die before reaching retirement age, you can ensure the financial well-being of your surviving beneficiaries.

The most common vehicle for shifting retirement plan assets at retirement is an individual retirement account (IRA). Upon reaching retirement, you can roll over your retirement plan assets into an IRA. If you die before reaching retirement age or before you establish an IRA account, your designated beneficiary of your retirement plan may be able to roll the assets into an IRA as well. Typically when choosing beneficiaries an IRA owner may name a spouse, child, trust, or charity as a beneficiary of his or her IRA.

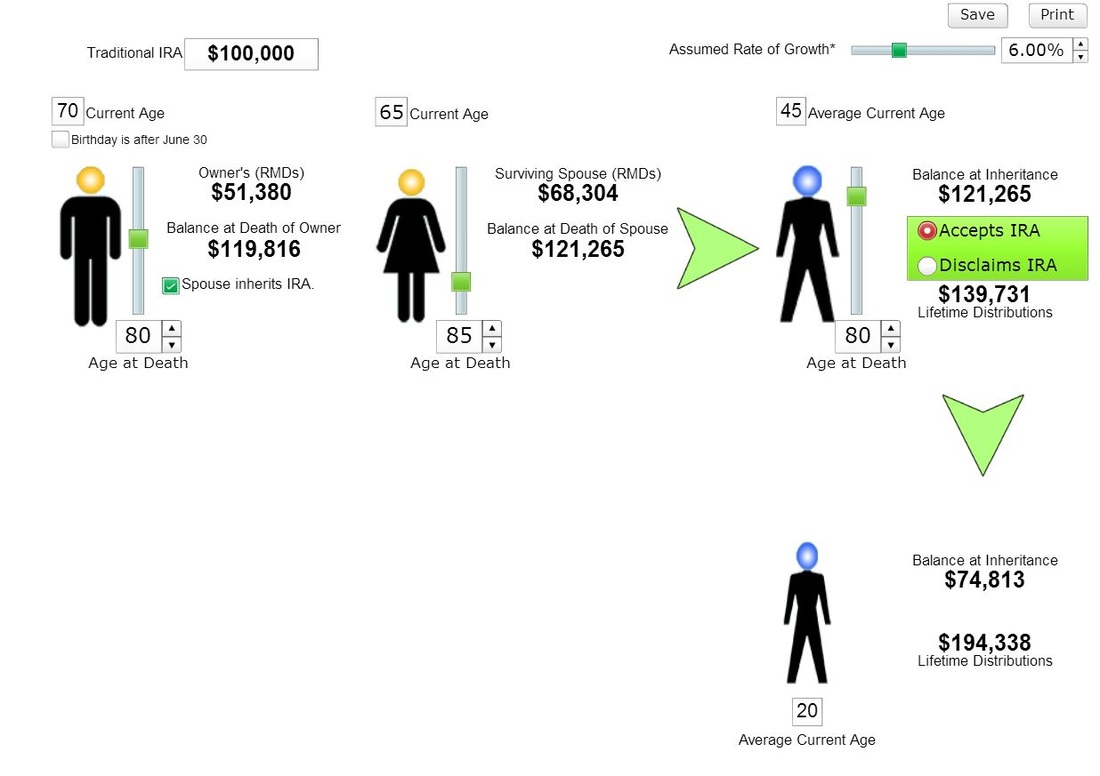

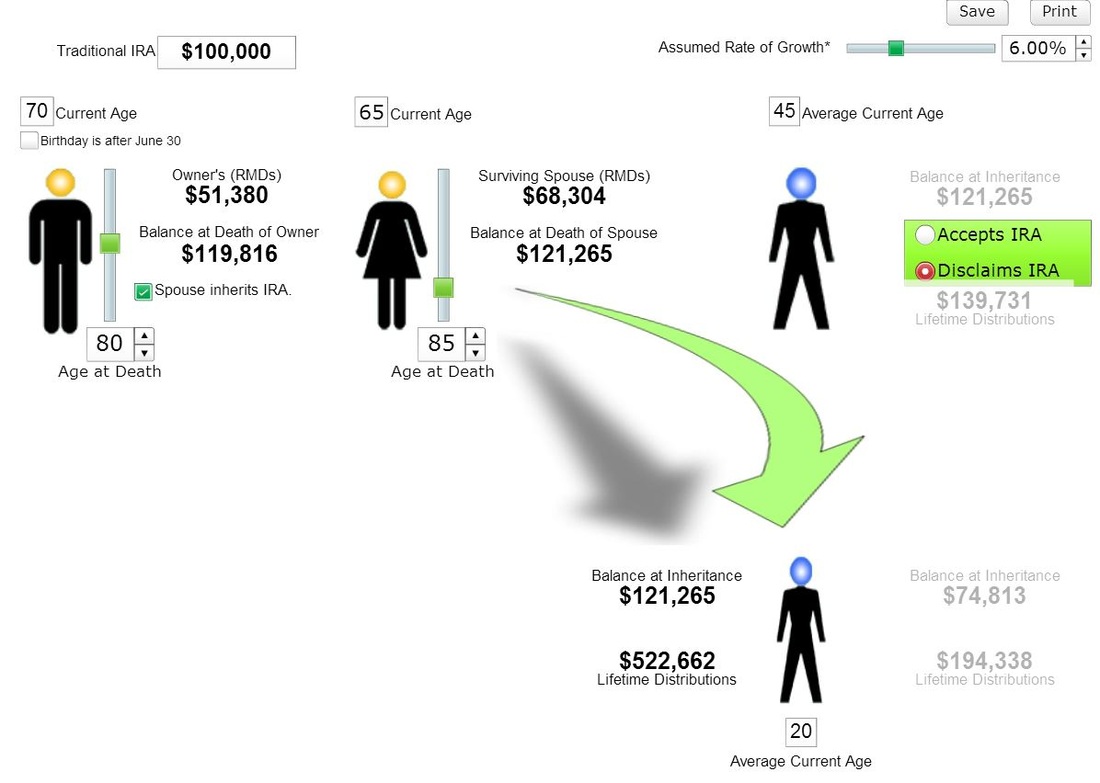

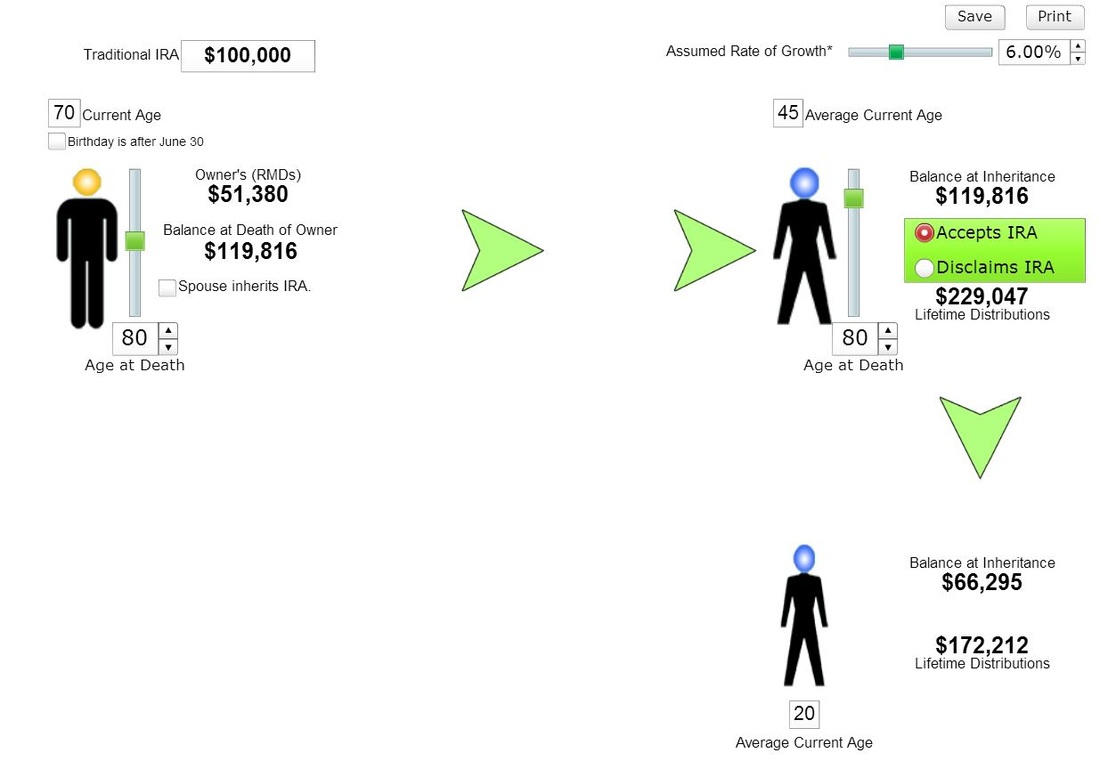

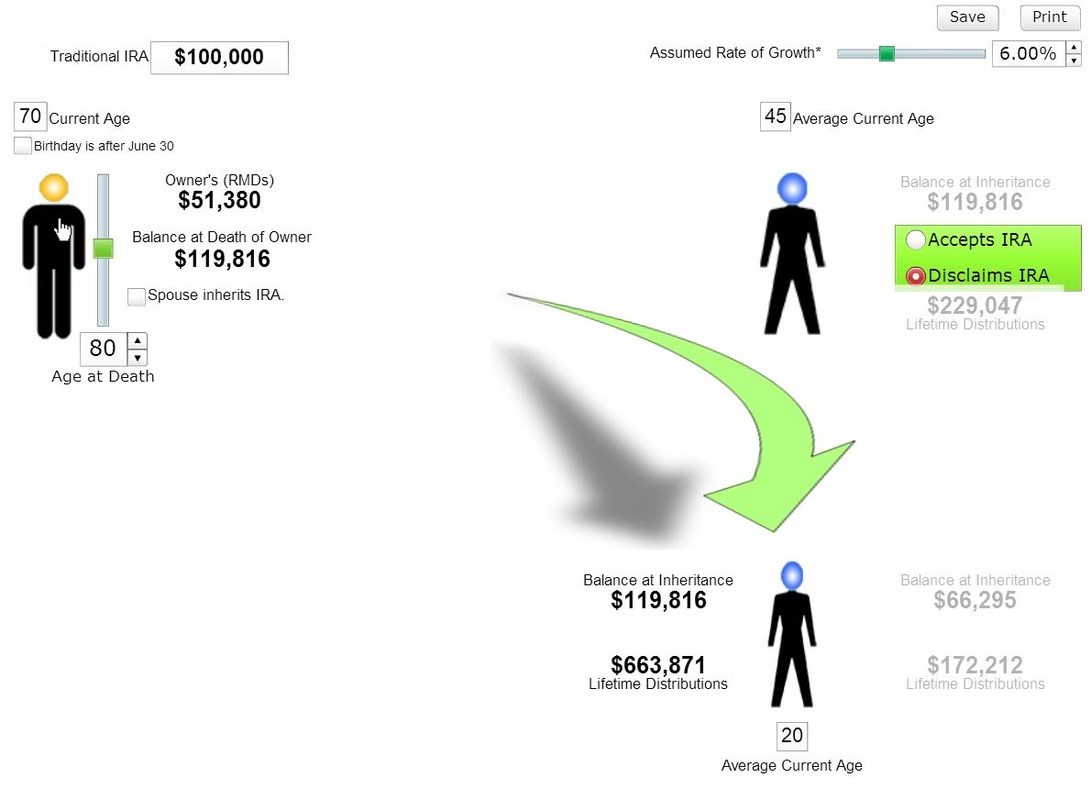

IRA Distribution Models

What model is best for you? It depends upon your goals and strategies.

Give us a call and let us run you a complimentary report.

Give us a call and let us run you a complimentary report.

|

IRA Owner

Spouse - Kids - Grandkids

|

IRA Owner

Spouse - Grandkids

|

IRA Owner

Kids - grandkids

|

IRA Owner

grandkids

|

Click on the images above to enlarge