|

CD vs Annuity Comparison

If you're debating whether the best place for your money is a certificate of deposit (CD) or deferred fixed annuity, the answer depends upon your individual financial situation and investment objectives. Both CDs and deferred fixed annuities are savings vehicles used to accumulate wealth. However, these two products are quite different; each has its own unique strengths and uses. For the sake of comparison, let's look at two similar versions of these products — an individually owned, Non–Qualified bank CD and an individually owned, Non–Qualified single premium deferred fixed annuity earning an annually renewable fixed rate of return.

How do CD's and Annuities compare?

Watch this video that explains the differences than you can explore more types of annuities on our website. MORE INFO

|

|

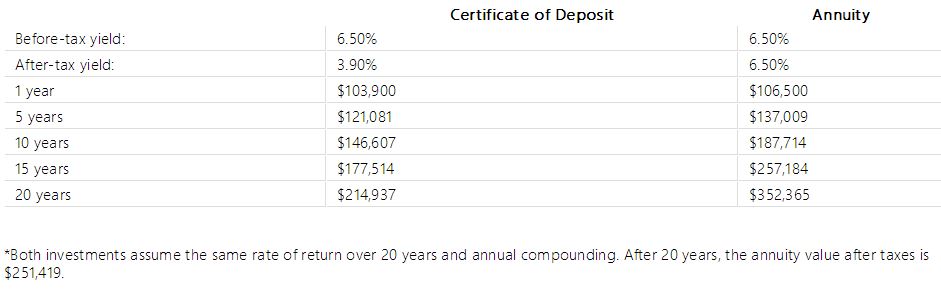

Assume an individual has $100,000 to invest and is considering an annuity or a CD. He or she is a 40% (combined state and federal) taxpayer. The following shows how tax deferral gives the annuity a significant advantage over the CD.*

|

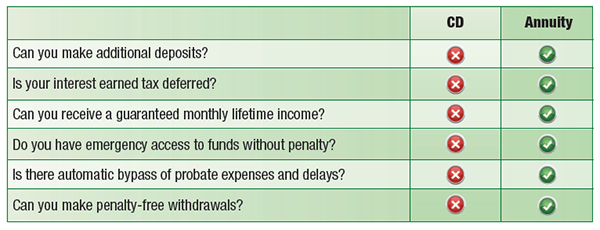

WHAT ARE CD'S

In the past, many comparisons have been made between certificates of deposit (CDs) and annuities. Some of these comparisons are fair and accurate; some are not. Let’s try to set the record straight. A CD is a time deposit insured by the FDIC guarantee that protects such bank assets with a limit of $1 million. Certificates of deposit should be viewed as short-term investments in that their yields are based on short-term assets. While maturities typically extend out to 5 years, most CD customers elect one-year or three-year time horizons. The earnings on CDs are taxable unless the product is held in a qualified account. Finally, CDs carry a loss-of-interest penalty that extends for the full term of the contract if it is cashed in before it matures. |

WHAT ARE ANNUITIES

An annuity is not a short-term investment. It rewards the buyer who commits to tax deferral and that reward is more dramatic every year. The annuity is not guaranteed by the FDIC, but there is no limit in terms of protection by the insurance company. The annuity has a finite period during which surrender charges apply. Unlike CDs, annuity monies are invested by the insurer for 3 to 10 years, depending on the terms of the contract. The annuity offers liquidity in addition to tax deferral through free withdrawals, loans and surrender charge waivers under certain circumstances. Finally, whereas the value of a CD could be part of the owner’s estate at death, the annuity passes outside of probate to the named beneficiary (assuming the beneficiary is an individual, not the estate). |

Click to Download your copy of this document

|

|